Interest rates might sound like a boring topic, but trust me, they’re a big deal in your financial life. Whether you’re saving money, borrowing for a house, or even just swiping that credit card, interest rates play a role in how much you earn or pay. Think of them as the invisible hands shaping your wallet’s fate. If you’re clueless about how they work, don’t sweat it—we’ve got you covered.

Let’s face it, most people don’t wake up thinking about interest rates, but they affect your daily life more than you realize. From the cost of loans to the return on your savings, these rates can either work in your favor or hit your pocket hard. Understanding them is like having a cheat code to managing your finances better.

In this article, we’ll break down everything you need to know about interest rates. We’ll cover the basics, how they’re set, their impact on the economy, and some tips to make them work for you. So, grab a coffee, and let’s dive into the world of interest rates without the finance jargon.

What Exactly Are Interest Rates?

Alright, so what’s the deal with interest rates? Simply put, they’re the cost of borrowing money or the reward for lending it. Imagine you take out a loan from the bank; the interest rate is the percentage of that loan you’ll have to pay back on top of the original amount. On the flip side, if you deposit money into a savings account, the interest rate is the percentage the bank pays you for keeping your cash there.

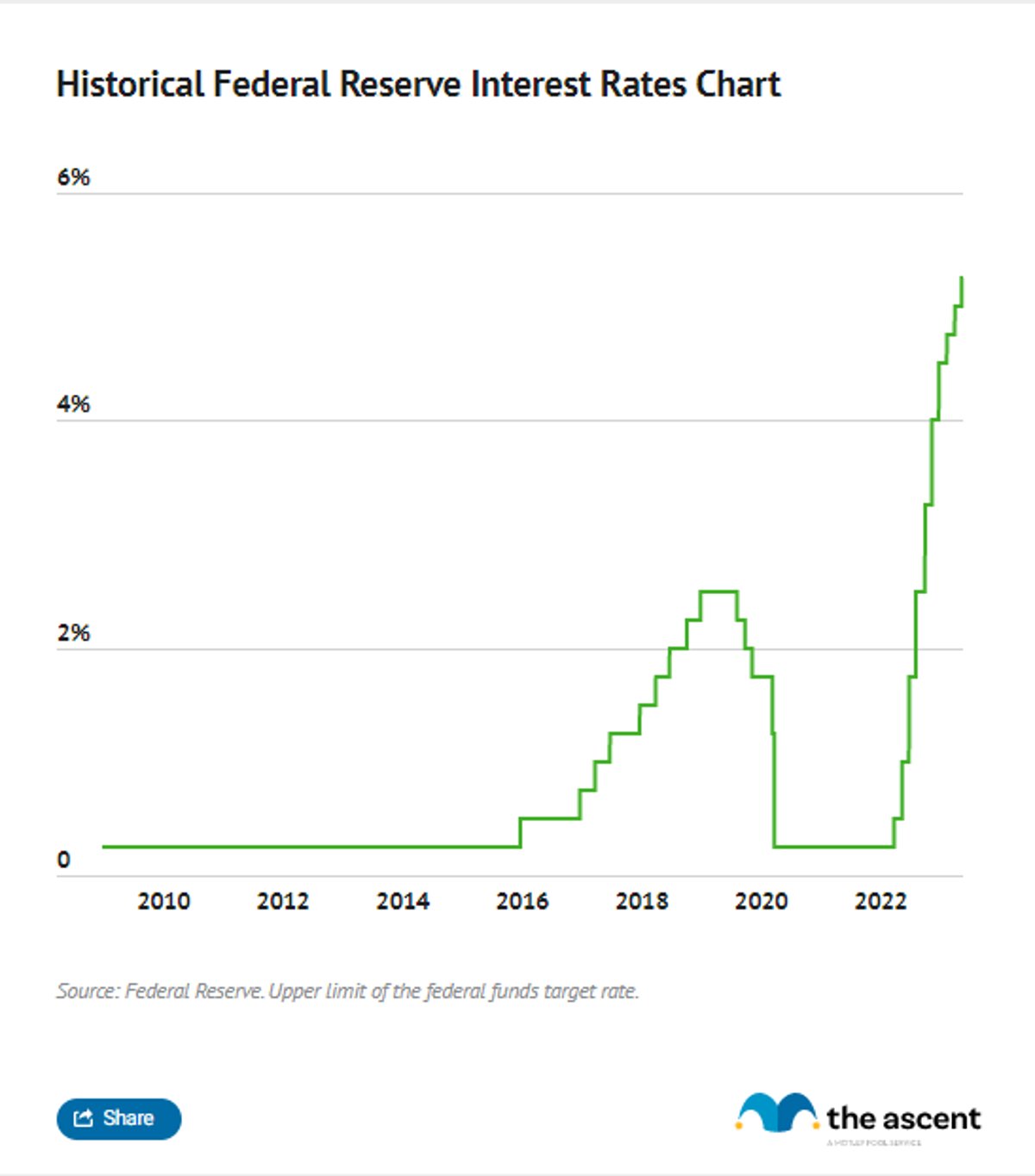

Interest rates are like the price tag of money. They’re set by central banks, like the Federal Reserve in the U.S., and influence everything from mortgage payments to credit card bills. And yeah, they’re not just random numbers—they’re carefully calculated based on economic conditions and goals.

How Are Interest Rates Determined?

Now, you might be wondering, who decides these magical numbers? The answer lies in central banks. In the U.S., the Federal Reserve plays a key role in setting interest rates. They adjust them to control inflation, manage economic growth, and keep unemployment in check. It’s like a balancing act where too high or too low rates can cause chaos.

Here’s the breakdown:

- Inflation Control: If prices are rising too fast, central banks might raise interest rates to slow spending.

- Economic Growth: During a recession, they might lower rates to encourage borrowing and spending.

- Unemployment: Lower rates can stimulate job creation by making it cheaper for businesses to borrow and invest.

Types of Interest Rates You Should Know

Not all interest rates are created equal. There are different kinds that affect various aspects of your financial life. Let’s break them down:

1. Prime Interest Rate

This is the rate banks charge their best customers—usually big corporations or super-wealthy individuals. It’s like the gold standard of interest rates and often serves as a benchmark for other rates. If you hear about changes in the prime rate, it’s a good indicator of what’s happening in the broader economy.

2. Federal Funds Rate

The Federal Funds Rate is the interest rate banks charge each other for overnight loans. The Federal Reserve sets a target range for this rate, which influences all other rates in the economy. Think of it as the foundation upon which other rates are built.

3. Mortgage Rates

If you’re planning to buy a house, mortgage rates are a big deal. These are the interest rates you pay on home loans. They’re influenced by the Federal Funds Rate, but also by factors like your credit score and the overall housing market. A small change in mortgage rates can mean thousands of dollars over the life of a loan.

4. Credit Card Interest Rates

Ever notice how your credit card bill seems to grow faster than your hair? That’s because credit card interest rates are often sky-high. They’re usually variable, meaning they can change based on the prime rate. If you carry a balance, those rates can really add up.

How Interest Rates Affect the Economy

Interest rates don’t just impact individuals—they have a massive effect on the overall economy. When rates are low, borrowing becomes cheaper, which can boost spending and investment. Conversely, high rates can slow down economic activity by making loans more expensive. It’s like a seesaw where the central bank adjusts the weight to keep things balanced.

Impact on Businesses

For businesses, interest rates influence everything from hiring decisions to expansion plans. Lower rates make it easier for companies to borrow money for projects, which can lead to job creation and economic growth. On the flip side, high rates can force businesses to cut back on spending, which can lead to layoffs.

Impact on Consumers

As a consumer, interest rates affect your wallet in multiple ways. Low rates can mean cheaper loans for big-ticket items like cars and houses, but they can also reduce the return on your savings. High rates, on the other hand, can increase the cost of borrowing but boost the interest you earn on savings accounts.

Understanding Compound Interest

Compound interest is like the superhero of interest rates—it can either be your best friend or your worst enemy. It’s the interest earned or charged on both the initial amount and the accumulated interest from previous periods. In simple terms, it’s interest on top of interest.

Here’s why it matters:

- Savings: Compound interest can help your money grow exponentially over time. The earlier you start saving, the more you benefit.

- Loans: On the flip side, compound interest can make debt snowball out of control if you don’t pay it off quickly.

How to Calculate Compound Interest

Don’t worry, you don’t need a PhD in math to figure this out. There’s a simple formula:

A = P(1 + r/n)^(nt)

Where:

- A = the future value of the investment/loan, including interest

- P = the principal amount (initial deposit or loan amount)

- r = the annual interest rate (decimal)

- n = the number of times interest is compounded per year

- t = the number of years the money is invested or borrowed for

Strategies to Make Interest Rates Work for You

Now that you know the basics, let’s talk about how to use interest rates to your advantage. Here are a few tips:

1. Shop Around for Better Rates

Whether you’re getting a loan or opening a savings account, don’t settle for the first offer you see. Compare rates from different banks and lenders to find the best deal. It’s like bargain hunting, but for your finances.

2. Pay Off High-Interest Debt First

If you’re juggling multiple debts, focus on paying off the ones with the highest interest rates first. This strategy, called the avalanche method, can save you a ton of money in the long run.

3. Take Advantage of Low Rates

When interest rates are low, it’s a great time to borrow for big purchases like a house or car. Just make sure you can afford the payments, even if rates go up in the future.

Common Misconceptions About Interest Rates

There are a lot of myths floating around about interest rates. Let’s debunk a few:

1. Lower Rates Always Mean Cheaper Loans

Not necessarily. Other factors, like fees and terms, can affect the total cost of a loan. Always read the fine print before signing on the dotted line.

2. Interest Rates Only Affect Borrowers

Wrong! Savers are impacted too. High interest rates can mean better returns on savings accounts, while low rates can reduce those returns.

3. Rates Stay the Same for Long Periods

Interest rates are constantly changing based on economic conditions. What’s true today might not be tomorrow, so stay informed.

Future Trends in Interest Rates

So, what’s the crystal ball saying about interest rates? Experts predict they’ll continue to fluctuate based on global economic conditions. With factors like inflation, trade tensions, and technological advancements influencing the market, it’s hard to say exactly where rates are headed. But one thing’s for sure—they’ll remain a crucial part of the financial landscape.

How Technology Is Shaping Interest Rates

Technology is playing a bigger role in how interest rates are set and managed. Algorithms and AI are being used to analyze data and predict trends, making the process more efficient. This means rates could become even more dynamic in the future, responding faster to changes in the economy.

Conclusion: Take Control of Your Financial Future

Interest rates might seem like a complicated topic, but they’re an essential part of your financial life. By understanding how they work and how to make them work for you, you can take control of your money and plan for a brighter future.

So, here’s the deal: don’t just sit there and let interest rates control you. Do your research, compare rates, and make informed decisions. And remember, if you’re ever feeling overwhelmed, there’s no shame in seeking advice from a financial expert.

Now, it’s your turn. Leave a comment below and let us know what you think about interest rates. Are they your friend or foe? And don’t forget to share this article with your friends so they can get savvy about their finances too!

![Buying a Home? Mortgage Rate Guide for Singapore [2023]](https://blog.roshi.sg/wp-content/uploads/2022/08/Singapore-Home-Loan-Rates-2022.jpeg)