Interest rates today are more than just numbers—they're the heartbeat of the global economy. Whether you're a first-time homebuyer, an investor looking to grow your wealth, or someone simply trying to make ends meet, understanding interest rates is crucial. It's like having a map when you're navigating uncharted territory. So, buckle up because we're diving deep into the world of interest rates and uncovering what they mean for you.

Let’s be real, folks. Interest rates can feel like this mysterious force that controls everything from mortgage payments to credit card bills. But here's the thing—they don’t have to stay a mystery. By the time you finish reading this article, you'll know exactly how interest rates work, why they matter, and how to use them to your advantage.

We’re not just throwing random facts at you. This guide is packed with actionable insights, expert tips, and real-world examples to help you navigate the ever-changing financial landscape. So, whether you’re saving for retirement or thinking about taking out a loan, this is your go-to resource for all things interest rates today.

Table of Contents

- What Are Interest Rates?

- Current Interest Rates Today

- Factors Affecting Interest Rates

- Impact on the Economy

- Effects on Personal Finance

- Investment Opportunities

- Historical Trends of Interest Rates

- Role of Central Banks

- Future Outlook for Interest Rates

- Conclusion: Taking Control of Your Financial Future

What Are Interest Rates?

Alright, let’s break it down. Interest rates are essentially the cost of borrowing money. Think of it as rent for using someone else’s cash. When you take out a loan or use a credit card, the lender charges you interest as a way to make a profit. On the flip side, when you deposit money in a savings account, the bank pays you interest as a reward for keeping your money there.

Interest rates come in different shapes and sizes. You’ve got fixed rates, variable rates, prime rates, and benchmark rates. Each one serves a specific purpose and affects different parts of the economy. For example, the Federal Reserve sets a benchmark rate that influences everything from mortgage rates to car loans.

Why Do Interest Rates Matter?

Interest rates matter because they impact almost every aspect of our lives. They affect how much we pay for loans, how much we earn on our savings, and even the overall health of the economy. When rates are low, borrowing becomes cheaper, which can stimulate spending and investment. But when rates are high, it can slow down economic growth by making borrowing more expensive.

Here’s a quick rundown of why interest rates are so important:

- They influence inflation and deflation.

- They determine the cost of borrowing for businesses and consumers.

- They affect the value of currencies on the global market.

- They play a key role in shaping monetary policy.

Current Interest Rates Today

So, what’s the scoop on interest rates today? As of [insert current date], rates have been on a bit of a rollercoaster ride. The Federal Reserve has been adjusting rates to combat inflation while also supporting economic growth. It’s a delicate balancing act that affects everyone from Wall Street tycoons to Main Street families.

Here’s a snapshot of some key interest rates right now:

- Federal Funds Rate: [Insert current rate]

- Prime Rate: [Insert current rate]

- Mortgage Rates: [Insert current rate]

- Car Loan Rates: [Insert current rate]

Keep in mind that these rates can fluctuate based on a variety of factors, including economic data, geopolitical events, and central bank decisions. So, it’s always a good idea to stay informed and keep an eye on the latest trends.

Factors Affecting Interest Rates

Interest rates don’t just happen—they’re influenced by a complex mix of factors. Here are some of the biggest players:

Economic Growth

When the economy is booming, interest rates tend to rise. This is because higher growth often leads to increased demand for loans, which drives up rates. Conversely, during a recession, rates may drop to encourage borrowing and stimulate the economy.

Inflation

Inflation is like the big brother of interest rates. When prices go up, central banks often raise rates to keep things in check. This helps prevent the economy from overheating and ensures that purchasing power remains stable.

Monetary Policy

Central banks, like the Federal Reserve, play a huge role in setting interest rates. They use monetary policy tools to control the money supply and influence economic conditions. By raising or lowering rates, they can either tighten or loosen the reins on the economy.

Impact on the Economy

Interest rates have a ripple effect throughout the economy. They influence everything from consumer spending to business investment. When rates are low, people are more likely to take out loans for big-ticket items like homes and cars. Businesses may also expand operations or invest in new projects.

On the flip side, high interest rates can slow down economic activity. Borrowing becomes more expensive, which can lead to decreased spending and investment. This can be a double-edged sword, as it helps control inflation but may also lead to job losses and reduced growth.

How Do Interest Rates Affect Housing Markets?

The housing market is particularly sensitive to interest rate changes. Mortgage rates directly impact how affordable it is to buy a home. When rates are low, more people can afford to purchase property, driving up demand and prices. But when rates rise, it can cool down the market and make homeownership less accessible for some buyers.

Effects on Personal Finance

Interest rates don’t just affect the big picture—they hit close to home, too. Here’s how they impact your personal finances:

Savings Accounts

If you’ve got money stashed away in a savings account, interest rates can work in your favor. Higher rates mean you earn more on your deposits, which is great for long-term savings goals. However, if rates are low, your money may not grow as quickly as you’d like.

Credit Cards

Credit card interest rates are usually tied to the prime rate, so any changes in that rate will affect your monthly payments. If rates go up, you’ll end up paying more in interest charges, which can make it harder to pay off balances.

Investment Opportunities

For investors, interest rates can create both challenges and opportunities. When rates are low, it can be a good time to invest in stocks or real estate, as borrowing costs are lower. But when rates rise, bonds and other fixed-income investments may become more attractive.

It’s all about finding the right balance and timing your moves wisely. Whether you’re a seasoned investor or just starting out, understanding how interest rates affect your portfolio is key to making smart financial decisions.

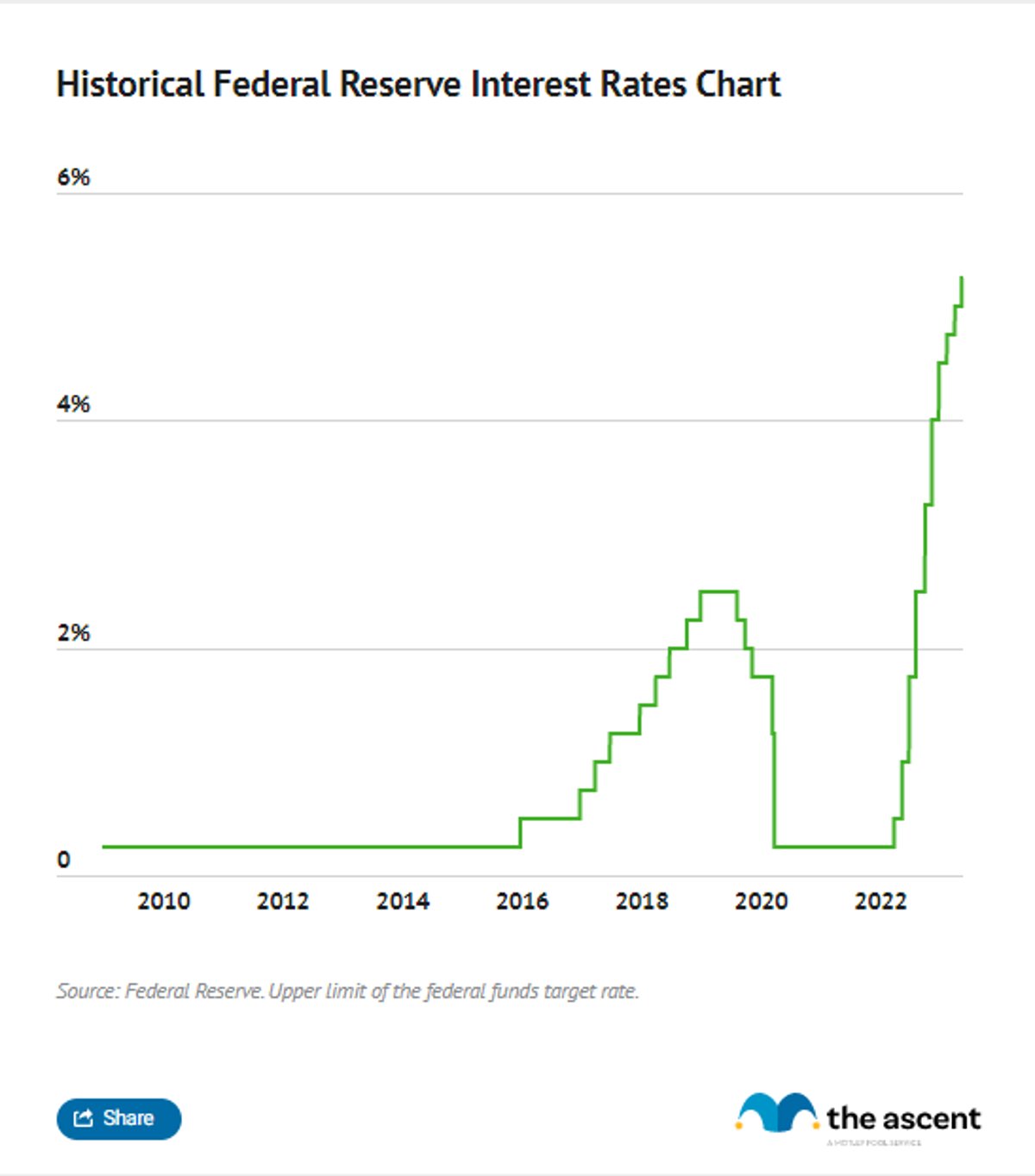

Historical Trends of Interest Rates

Looking back at history can give us valuable insights into where interest rates might be headed. Over the past few decades, we’ve seen some pretty dramatic swings in rates. For example, in the 1980s, interest rates were sky-high due to rampant inflation. But in recent years, rates have been historically low, thanks to efforts to stimulate economic recovery.

By studying these trends, we can better anticipate future movements and prepare accordingly. It’s like reading the tea leaves of the financial world—only with actual data to back it up.

Role of Central Banks

Central banks are the puppet masters of interest rates. They set the tone for monetary policy and influence everything from inflation to unemployment. Through tools like open market operations and reserve requirements, they can tighten or loosen the money supply as needed.

But it’s not all about numbers—central banks also play a crucial role in maintaining public confidence. By communicating clearly and transparently, they help stabilize expectations and reduce uncertainty in the markets.

Future Outlook for Interest Rates

So, where are interest rates headed next? That’s the million-dollar question, and the answer isn’t always clear. However, based on current trends and economic indicators, we can make some educated guesses.

Experts predict that rates may continue to rise in the near term as central banks work to combat inflation. But as the economy adjusts and growth stabilizes, rates could level off or even decline again. Of course, anything can happen, so it’s important to stay flexible and adapt to changing conditions.

Conclusion: Taking Control of Your Financial Future

Interest rates today are a powerful force shaping our financial lives. From mortgages to credit cards, they impact everything we do with money. By understanding how interest rates work and staying informed about current trends, you can take control of your financial future and make smarter decisions.

So, what’s your next move? Whether you’re saving, borrowing, or investing, remember that knowledge is power. Use the insights from this guide to navigate the ever-changing world of interest rates and build a brighter financial future for yourself and your family.

Don’t forget to share this article with your friends and family, and leave a comment below if you have any questions or thoughts. Together, we can all become smarter about money and make the most of what interest rates have to offer!