Hey there, let’s dive straight into the heart of the matter. Federal Reserve interest rates have been a buzzword in the financial world for decades, shaping economies and influencing everything from your mortgage payments to your savings account. Whether you're an investor, a homeowner, or simply someone trying to understand how the economy works, these rates are a game-changer. They're like the secret sauce in a recipe that keeps the economic machine running smoothly—or at least as smoothly as possible. So, buckle up, because we’re about to take a deep dive into the fascinating world of interest rates.

Now, you might be wondering, why should you care about the Federal Reserve’s interest rates? Well, here's the deal: these rates have a ripple effect on your daily life. From the cost of borrowing money to the return on your savings, the decisions made by the Federal Reserve impact both the global and local economies. Understanding them is like having a cheat code to the financial world. It gives you insight into how your money works for you—or against you.

Before we dive deeper, let’s set the stage. The Federal Reserve, often referred to as "the Fed," is not just some random group of economists sitting around a table. It’s the central banking system of the United States, and its primary goal is to maintain economic stability. And one of the most powerful tools in its arsenal? You guessed it—interest rates. So, whether you're a finance pro or just someone curious about the financial system, this article is for you.

What Are Federal Reserve Interest Rates?

Alright, let’s break it down. Federal Reserve interest rates, also known as the federal funds rate, are essentially the interest rates that banks charge each other for overnight loans. The Fed uses these rates as a tool to influence the economy. Think of it like a thermostat for the economy—if things are heating up too much, they’ll adjust the rates to cool things down, and vice versa.

But why does this matter? Well, when the Fed adjusts these rates, it affects everything from credit card interest rates to mortgage rates. It’s like a domino effect that touches nearly every aspect of the financial system. For instance, if the Fed lowers interest rates, borrowing becomes cheaper, encouraging spending and investment. On the flip side, raising rates can slow down spending and help control inflation.

How Do These Rates Work?

Here’s the deal: the Federal Reserve sets a target range for the federal funds rate. Banks then lend to each other within this range to meet their reserve requirements. If a bank has more reserves than it needs, it can lend to another bank that’s short on reserves. The interest rate charged on these loans is what we call the federal funds rate.

Now, here’s where it gets interesting. The Fed doesn’t directly control this rate. Instead, it influences it through open market operations, buying and selling government securities. By doing so, it can increase or decrease the money supply, which in turn affects interest rates. It’s like a giant game of supply and demand, but on a national scale.

The Importance of Federal Reserve Interest Rates

Let’s talk about why these rates are so crucial. They’re not just numbers on a screen; they’re powerful tools that shape the economy. For starters, they help control inflation. If the economy is overheating and prices are rising too quickly, the Fed can raise interest rates to slow things down. Conversely, if the economy is sluggish, lowering rates can stimulate growth.

But that’s not all. These rates also influence consumer behavior. When rates are low, people are more likely to borrow money for big purchases like homes and cars. Businesses are also more likely to invest in new projects. On the flip side, higher rates can discourage borrowing and encourage saving.

Impact on the Global Economy

Now, here’s the kicker: the Fed’s decisions don’t just affect the U.S. economy. They have a global impact. Many countries peg their currencies to the U.S. dollar, so changes in U.S. interest rates can affect currency values worldwide. This, in turn, can impact trade balances, investment flows, and even political stability in some regions.

For example, when the Fed raises rates, it can lead to a stronger dollar. This makes U.S. exports more expensive and imports cheaper, potentially affecting trade partners. It’s like a giant game of economic chess, where every move has consequences far beyond the borders of the U.S.

How Federal Reserve Interest Rates Affect You

Okay, let’s get personal. How do these rates affect your everyday life? Well, if you have a mortgage, car loan, or credit card, you’re probably already feeling the effects. When the Fed raises rates, the cost of borrowing goes up. This means higher monthly payments on your loans and credit cards. On the flip side, if you have savings, higher rates can mean better returns on your money.

But it’s not just about loans and savings. These rates can also affect your job prospects. When the economy slows down due to higher rates, companies may be less likely to hire. Conversely, when rates are low, businesses may expand, creating more job opportunities.

Real-Life Examples

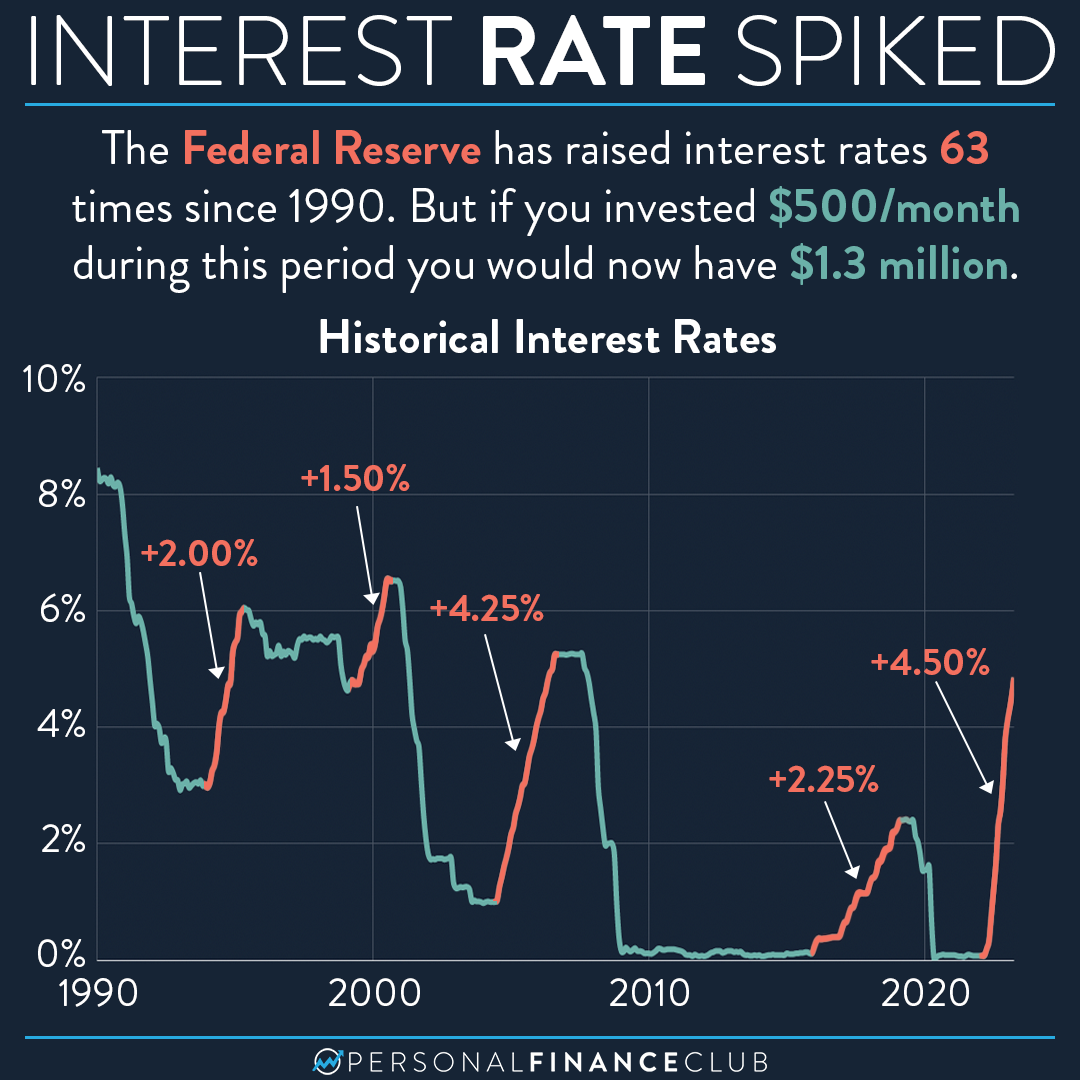

Let’s look at some real-life examples. In 2008, during the financial crisis, the Fed slashed interest rates to near zero to stimulate the economy. This helped prevent a total collapse and eventually led to a recovery. On the other hand, in the early 1980s, the Fed raised rates to record highs to combat runaway inflation. This led to a recession but ultimately helped stabilize the economy.

These examples show just how powerful the Fed’s tools can be. They’re not just numbers; they’re decisions that can shape the course of history.

The History of Federal Reserve Interest Rates

Now, let’s take a trip down memory lane. The Federal Reserve was established in 1913, but its role in setting interest rates has evolved over time. In the early days, the focus was on maintaining financial stability and preventing bank runs. Over the years, the Fed’s role has expanded to include controlling inflation and promoting maximum employment.

One of the most significant periods in Fed history was the 1970s and 1980s. During this time, inflation was rampant, and the Fed had to take drastic measures to bring it under control. Chairman Paul Volcker raised interest rates to unprecedented levels, leading to a recession but ultimately restoring economic stability.

Key Moments in Fed History

Here are some key moments in the Fed’s history:

- 1913: The Federal Reserve is established.

- 1970s: High inflation leads to aggressive rate hikes.

- 2008: Interest rates are slashed to near zero during the financial crisis.

- 2020: The Fed lowers rates to zero again during the pandemic.

These moments show how the Fed has adapted to changing economic conditions over the years.

Understanding the Federal Reserve’s Role

So, what exactly does the Fed do? Its primary responsibilities include conducting monetary policy, supervising and regulating banks, maintaining financial stability, and providing financial services. But when it comes to interest rates, its main goal is to promote price stability and maximum employment.

To achieve these goals, the Fed uses a variety of tools, including setting interest rates, conducting open market operations, and adjusting reserve requirements. It’s like having a toolbox full of options to tackle whatever economic challenges come its way.

Monetary Policy in Action

Monetary policy is the Fed’s way of influencing the economy. By adjusting interest rates and controlling the money supply, it can stimulate growth or slow down inflation. It’s like a balancing act, where the Fed has to weigh the benefits of growth against the risks of inflation.

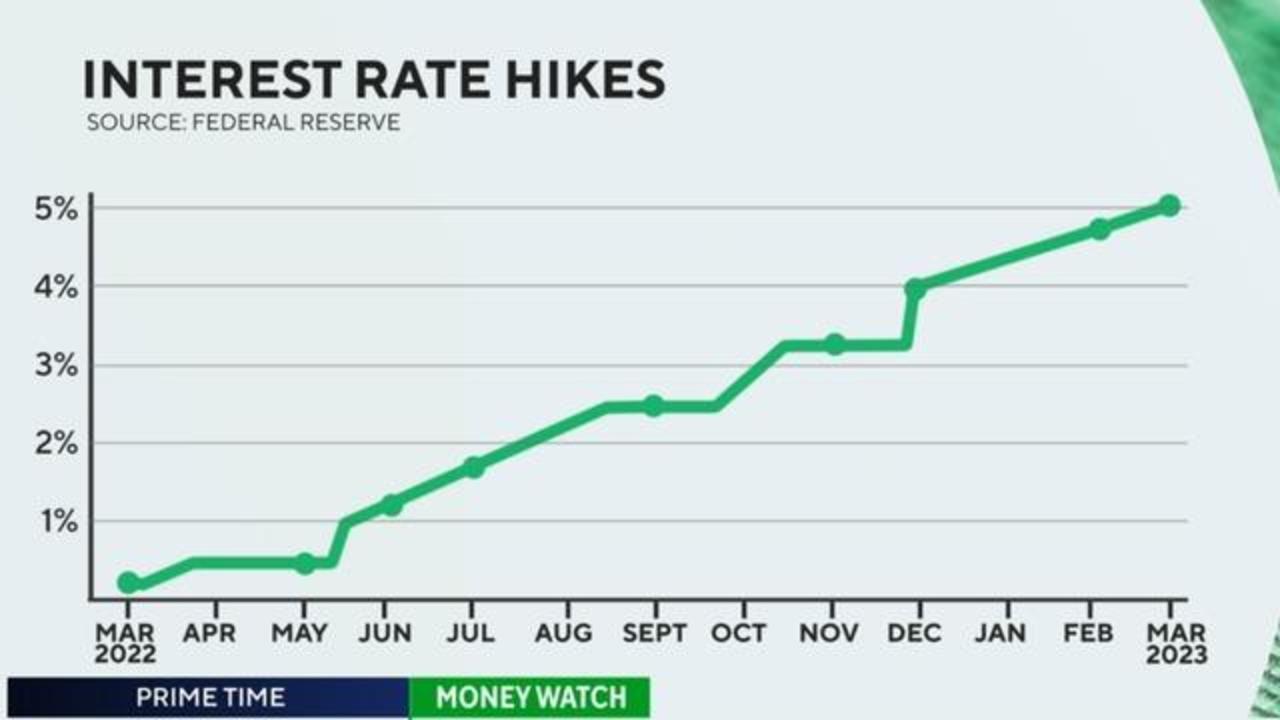

For example, during the pandemic, the Fed lowered interest rates to near zero and implemented quantitative easing to inject liquidity into the economy. This helped businesses stay afloat and kept unemployment from spiraling out of control.

Challenges Facing the Federal Reserve

Of course, the Fed isn’t without its challenges. One of the biggest is balancing the needs of different sectors of the economy. For example, while low interest rates can help stimulate growth, they can also lead to asset bubbles. Additionally, the Fed has to navigate political pressures and public opinion, which can sometimes be at odds with its goals.

Another challenge is global economic conditions. With the world becoming increasingly interconnected, the Fed has to consider how its decisions will affect other countries. This can sometimes lead to difficult trade-offs, where the best decision for the U.S. economy might not be the best for the global economy.

Future Directions

Looking ahead, the Fed will continue to face new challenges. Climate change, technological advancements, and demographic shifts are all factors that could impact the economy in the coming years. The Fed will need to adapt its tools and strategies to address these challenges and ensure long-term stability.

For example, some economists have suggested that the Fed may need to consider new tools, such as negative interest rates or digital currencies, to maintain its effectiveness in the future. It’s like preparing for the next level in a game, where the rules might change but the goal remains the same.

How to Prepare for Changes in Federal Reserve Interest Rates

So, how can you prepare for changes in interest rates? First, stay informed. Keep an eye on Fed announcements and economic indicators that might signal upcoming changes. Second, consider how these changes might affect your personal finances. If rates are expected to rise, it might be a good time to lock in a fixed-rate mortgage or pay down high-interest debt.

For investors, changes in interest rates can present both opportunities and risks. Rising rates can lead to higher returns on bonds, but they can also hurt stock prices. It’s important to diversify your portfolio and be prepared for volatility.

Strategies for Individuals

Here are some strategies you can use:

- Pay down high-interest debt when rates are low.

- Lock in fixed-rate loans before rates rise.

- Diversify your investment portfolio to manage risk.

- Consider alternative investments, such as real estate or commodities.

By taking these steps, you can position yourself to benefit from changes in interest rates rather than being caught off guard.

Conclusion

And there you have it—a deep dive into the world of federal reserve interest rates. From their role in shaping the economy to their impact on your daily life, these rates are a crucial part of the financial system. Whether you’re a homeowner, investor, or just someone trying to make sense of the economy, understanding them can give you a leg up in navigating the financial landscape.

So, what’s next? Take action! Stay informed, adjust your financial strategies, and be prepared for whatever the Fed throws your way. And don’t forget to share this article with your friends and family. Knowledge is power, and the more people understand how the financial system works, the better off we all are.

Table of Contents

- What Are Federal Reserve Interest Rates?

- The Importance of Federal Reserve Interest Rates

- How Federal Reserve Interest Rates Affect You

- The History of Federal Reserve Interest Rates

- Understanding the Federal Reserve’s Role

- Challenges Facing the Federal Reserve

- How to Prepare for Changes in Federal Reserve Interest Rates

Thanks for reading, and remember—knowledge is power!