Alright folks, let’s get real for a second. Interest rates today are more than just numbers on a screen or headlines in the news. They’re the heartbeat of our financial system, affecting everything from buying that dream house to paying off credit card debt. Whether you’re saving, borrowing, or investing, understanding interest rates is crucial if you want to make smart financial decisions. So buckle up, because we’re about to break it all down for you.

Let’s face it, the world of finance can be intimidating. Numbers flying around, percentages changing daily, and terms like "prime rate" or "Federal Reserve" thrown around like they’re common knowledge. But guess what? It doesn’t have to be that way. We’re here to simplify things for you and give you the tools to navigate the current interest rate landscape like a pro.

Whether you’re a first-time homebuyer wondering if now’s the right time to lock in a mortgage or an investor trying to figure out where to put your money, this article’s got you covered. We’ll dive into what interest rates are, why they matter, and how they impact your everyday life. So, grab a coffee (or maybe a stiff drink), and let’s get started.

Before we dive deep into the numbers and trends, here’s a quick overview of what you’ll find in this article:

- What Are Interest Rates?

- Why Do Interest Rates Change?

- Current Interest Rates Today

- How Interest Rates Affect You

- The Federal Reserve’s Role in Interest Rates

- Historical Interest Rate Trends

- Tips for Navigating Interest Rates

- Common Mistakes to Avoid

- Future Predictions for Interest Rates

- Final Thoughts on Interest Rates Today

What Are Interest Rates?

First things first, let’s start with the basics. Interest rates are essentially the cost of borrowing money or the reward for lending it. Think of it like this: when you take out a loan, the lender charges you interest as a fee for letting you use their cash. On the flip side, if you deposit money in a savings account, the bank pays you interest for keeping your cash in their vault.

Interest rates can be expressed in different ways, but the most common is an annual percentage rate (APR). This tells you how much you’ll pay or earn over the course of a year. For example, if you borrow $10,000 at a 5% interest rate, you’ll owe an extra $500 in interest by the end of the year. Simple, right?

How Are Interest Rates Determined?

Interest rates aren’t just plucked out of thin air. They’re influenced by a variety of factors, including:

- Economic conditions: If the economy’s booming, interest rates might rise to prevent overheating. If it’s struggling, rates might drop to encourage spending.

- Inflation: Higher inflation often leads to higher interest rates to keep the economy in check.

- Federal Reserve policies: The central bank plays a massive role in setting benchmark rates, which then trickle down to consumers.

Now that we’ve got the basics down, let’s move on to the juicy stuff: why interest rates keep changing.

Why Do Interest Rates Change?

Interest rates aren’t static—they’re constantly shifting in response to what’s happening in the economy. Think of them like a seesaw: when one side goes up, the other goes down. Here are some key reasons why interest rates today might be different from yesterday:

Economic Growth

When the economy’s growing strong, businesses are hiring, and consumers are spending. To keep things from getting out of control, the Federal Reserve might raise interest rates to cool things off. It’s like turning down the heat on a simmering pot.

Inflation

Inflation is the enemy of stable interest rates. If prices are rising too fast, the Fed will often hike rates to make borrowing more expensive and encourage saving. It’s their way of keeping the economy balanced.

Global Events

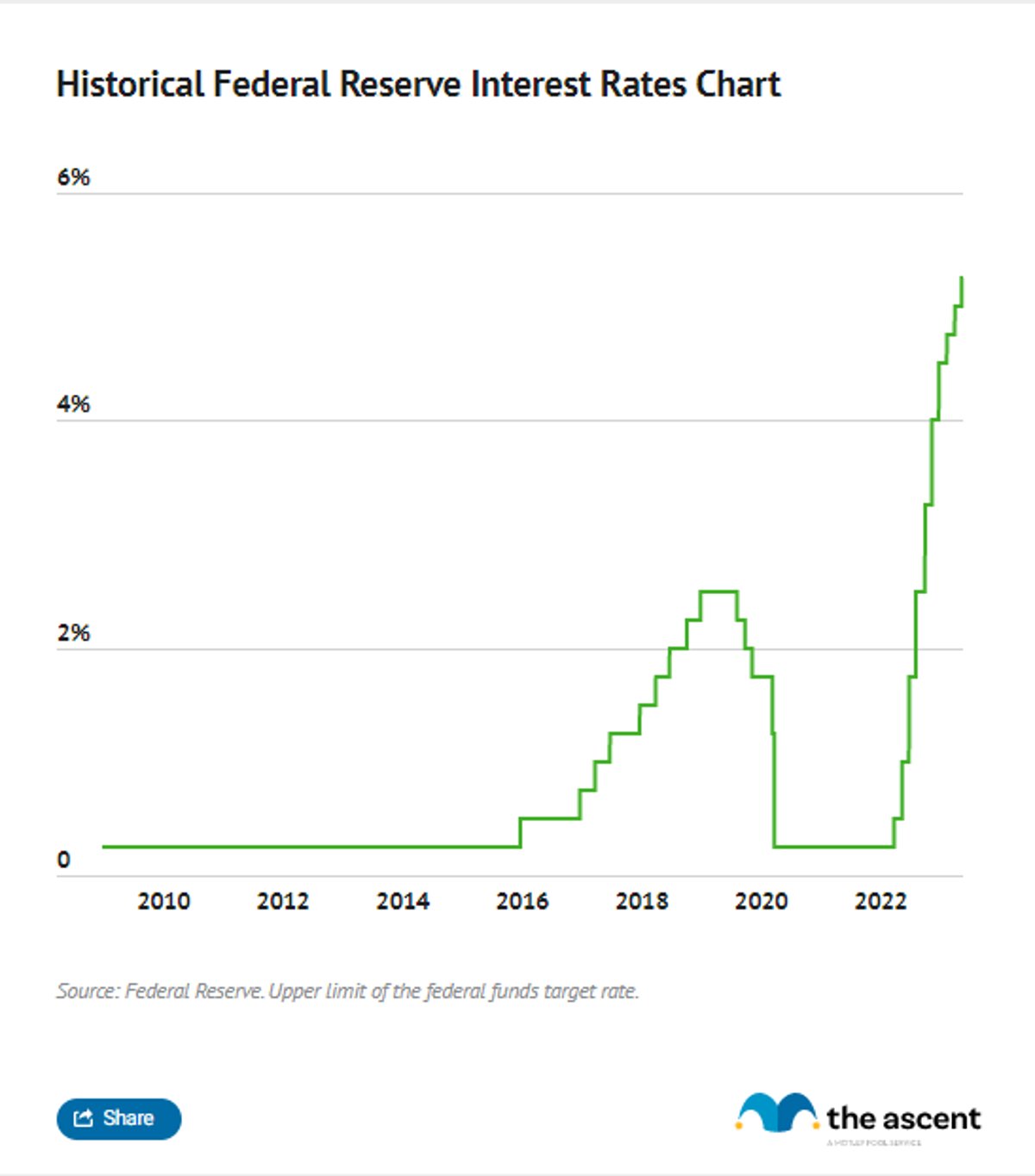

Let’s not forget about the world stage. Wars, pandemics, and geopolitical tensions can all impact interest rates. For example, during the COVID-19 pandemic, rates were slashed to near zero to stimulate the economy. But as things stabilized, they started creeping back up.

Current Interest Rates Today

Alright, let’s talk about the here and now. As of [insert current year], interest rates are sitting at [insert current rate]. But what does that mean for you? Let’s break it down:

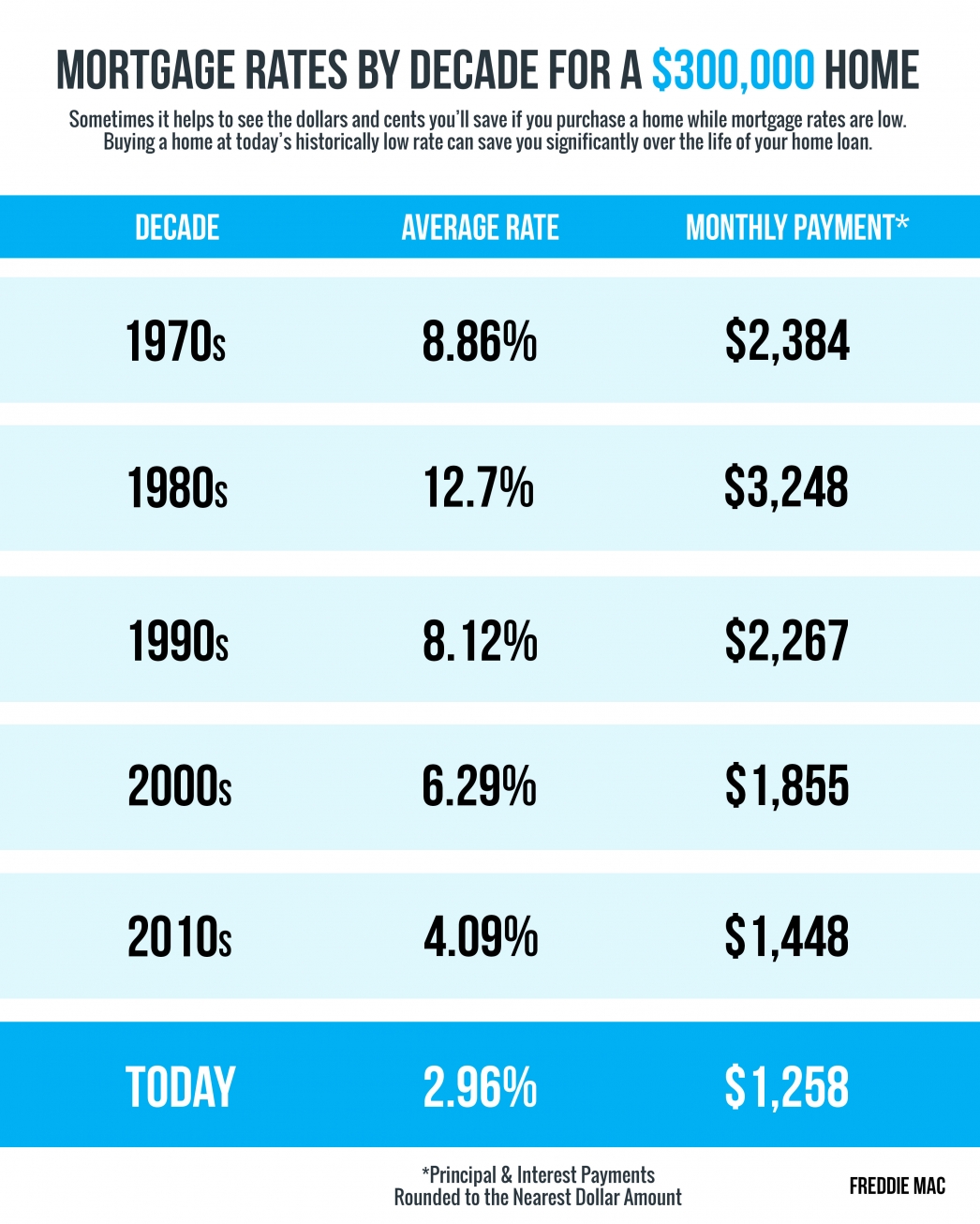

- Mortgage Rates: If you’re thinking about buying a home, mortgage rates are a big deal. Right now, they’re hovering around [insert rate], which means locking in a fixed-rate loan could save you big bucks in the long run.

- Savings Accounts: On the flip side, if you’re saving, you might be seeing higher returns on your deposits. Some banks are offering [insert rate] on savings accounts, which is a nice perk for savers.

- Credit Cards: Unfortunately, higher interest rates also mean higher credit card APRs. If you’re carrying a balance, now might be a good time to pay it off or transfer it to a card with a lower rate.

How Interest Rates Affect You

Interest rates today don’t just live in some abstract financial world—they have real-world consequences for your wallet. Here’s how they can impact you:

Buying a Home

If you’re in the market for a house, interest rates are a big deal. A small change in the rate can mean thousands of dollars in extra payments over the life of your mortgage. For example, a 30-year fixed-rate mortgage at 4% vs. 5% could mean a difference of tens of thousands of dollars.

Investing

Investors also need to pay attention to interest rates. Higher rates can make bonds more attractive, while lower rates might push investors into riskier assets like stocks. It’s all about finding the right balance for your portfolio.

The Federal Reserve’s Role in Interest Rates

Let’s talk about the big player in all of this: the Federal Reserve. The Fed sets the benchmark interest rate, which influences everything from credit card rates to mortgage rates. They meet several times a year to decide whether to raise, lower, or keep rates the same. Their decisions are based on a mix of economic data, inflation trends, and global events.

How the Fed Impacts You

When the Fed raises rates, borrowing becomes more expensive. This can slow down consumer spending and business investment, which might lead to slower economic growth. On the flip side, when rates are lowered, borrowing becomes cheaper, which can stimulate the economy.

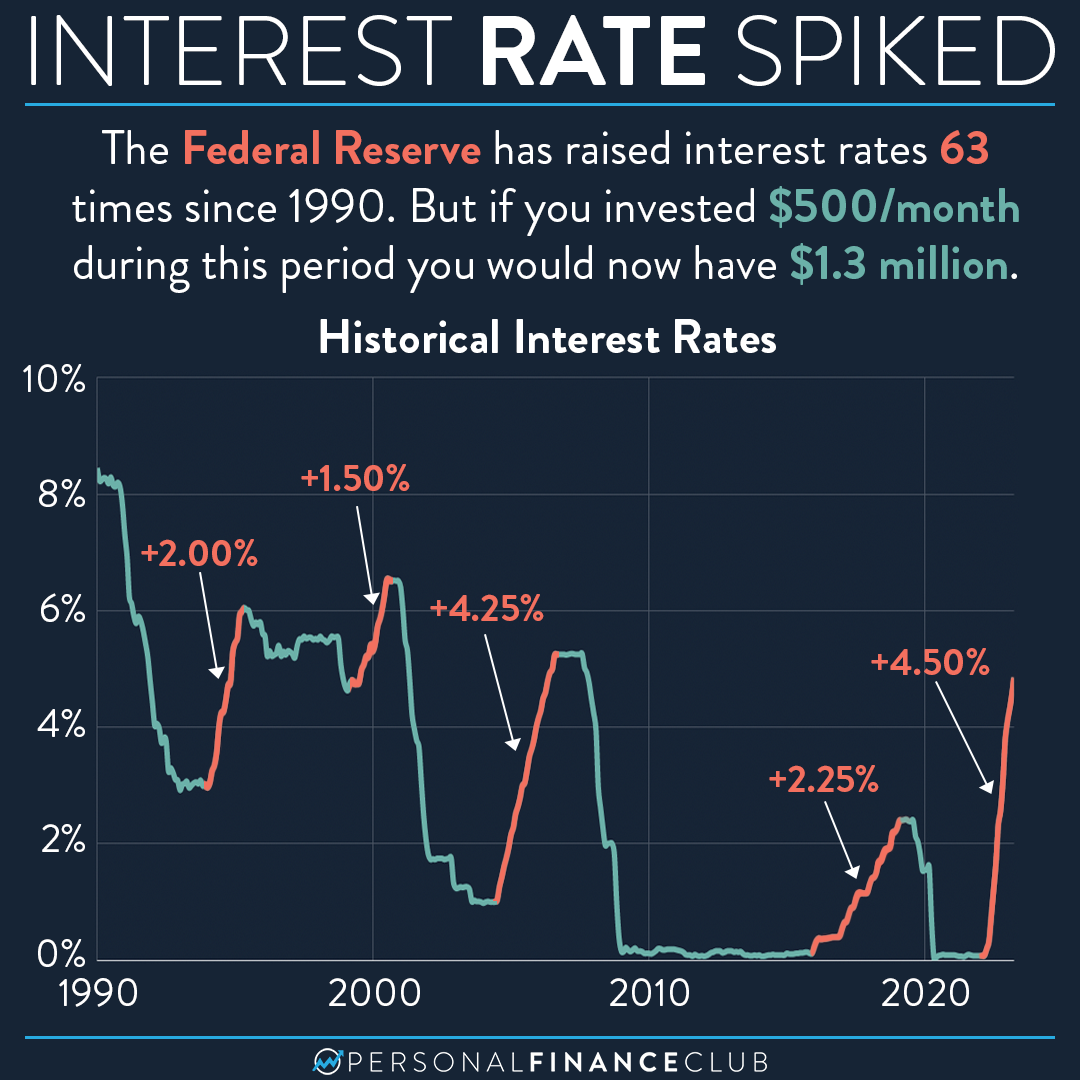

Historical Interest Rate Trends

Interest rates haven’t always been where they are today. Let’s take a trip down memory lane and see how they’ve evolved over the years:

The 1980s: Sky-High Rates

In the 1980s, interest rates were through the roof, with mortgage rates topping 18%. This was a response to runaway inflation, and the Fed had to take drastic measures to bring things under control.

The 2000s: Low Rates and the Housing Bubble

Fast forward to the early 2000s, and rates were much lower. This led to a housing boom, which eventually turned into a bust when the bubble burst in 2008. The Fed slashed rates to near zero to help stabilize the economy.

Today: A Mixed Bag

Right now, interest rates are in a bit of a sweet spot. They’re not too high, but they’re not too low either. This gives the economy room to grow without overheating. But as always, things can change in a heartbeat.

Tips for Navigating Interest Rates

So, how can you make the most of the current interest rate environment? Here are a few tips:

- Lock in Low Rates: If you’re borrowing, now might be a good time to lock in a fixed-rate loan before rates go up.

- Shop Around: Don’t settle for the first rate you see. Compare offers from different lenders to get the best deal.

- Pay Down Debt: If you’re carrying high-interest debt, focus on paying it off quickly to save money in the long run.

Common Mistakes to Avoid

While navigating interest rates today, there are a few common pitfalls to watch out for:

- Ignoring Rates: Don’t stick your head in the sand. Keep an eye on rate changes and adjust your financial strategy accordingly.

- Overborrowing: Just because rates are low doesn’t mean you should take on more debt than you can handle.

- Not Planning Ahead: Think about the long-term impact of interest rates on your financial goals and plan accordingly.

Future Predictions for Interest Rates

So, where are interest rates headed? Experts predict that rates will continue to rise slowly over the next few years as the economy recovers from recent challenges. However, a lot depends on inflation, global events, and the Fed’s decisions. It’s a bit like predicting the weather—there’s always a chance of surprises.

Final Thoughts on Interest Rates Today

Interest rates today are a critical piece of the financial puzzle. They impact everything from your mortgage to your savings account, and understanding them is key to making smart financial decisions. Whether you’re borrowing, saving, or investing, staying informed about rate changes can help you navigate the ever-changing economic landscape.

So, what’s your next move? Are you planning to lock in a mortgage, pay down debt, or invest in new opportunities? Whatever it is, make sure you’re making the most of the current interest rate environment. And don’t forget to share this article with your friends and family—it’s knowledge that can save them money too!

Got questions or comments? Drop them below, and let’s keep the conversation going. Your financial future is in your hands, and we’re here to help you every step of the way.