Interest rates play a pivotal role in shaping our financial lives, whether we're saving, borrowing, or investing. They're like the invisible hands that guide the economy, influencing everything from mortgage payments to credit card bills. If you've ever wondered why your loan repayments vary or why banks offer different rates on savings accounts, this article has got you covered. We'll break down the concept of interest rates in simple terms, so you can make smarter financial decisions.

Now, let's face it—interest rates aren't exactly the sexiest topic out there, but they're super important. Think of them as the unsung heroes of finance. They're the backbone of how money moves around the world, and understanding them can save you a ton of cash in the long run. Whether you're a first-time homebuyer or just trying to pay off student loans, knowing how interest rates work is key to managing your finances wisely.

So, buckle up because we're diving deep into the world of interest rates. From how they're determined to their impact on your wallet, we've got all the juicy details. And don't worry, we'll keep it real and conversational—no boring jargon here. Let's get started!

What Are Interest Rates Anyway?

Alright, let's start with the basics. Simply put, interest rates are the cost of borrowing money. When you take out a loan, the lender charges you interest as a fee for letting you use their cash. On the flip side, when you deposit money in a savings account, the bank pays you interest for keeping your money with them. It's a win-win situation, right? Well, sort of.

Interest rates are usually expressed as a percentage of the loan or deposit amount. For example, if you borrow $1,000 at an interest rate of 5%, you'll end up paying back $1,050. Easy peasy, right? But here's the catch—interest rates can vary depending on factors like the type of loan, your credit score, and even the state of the economy. So, it's not always as straightforward as it seems.

How Are Interest Rates Determined?

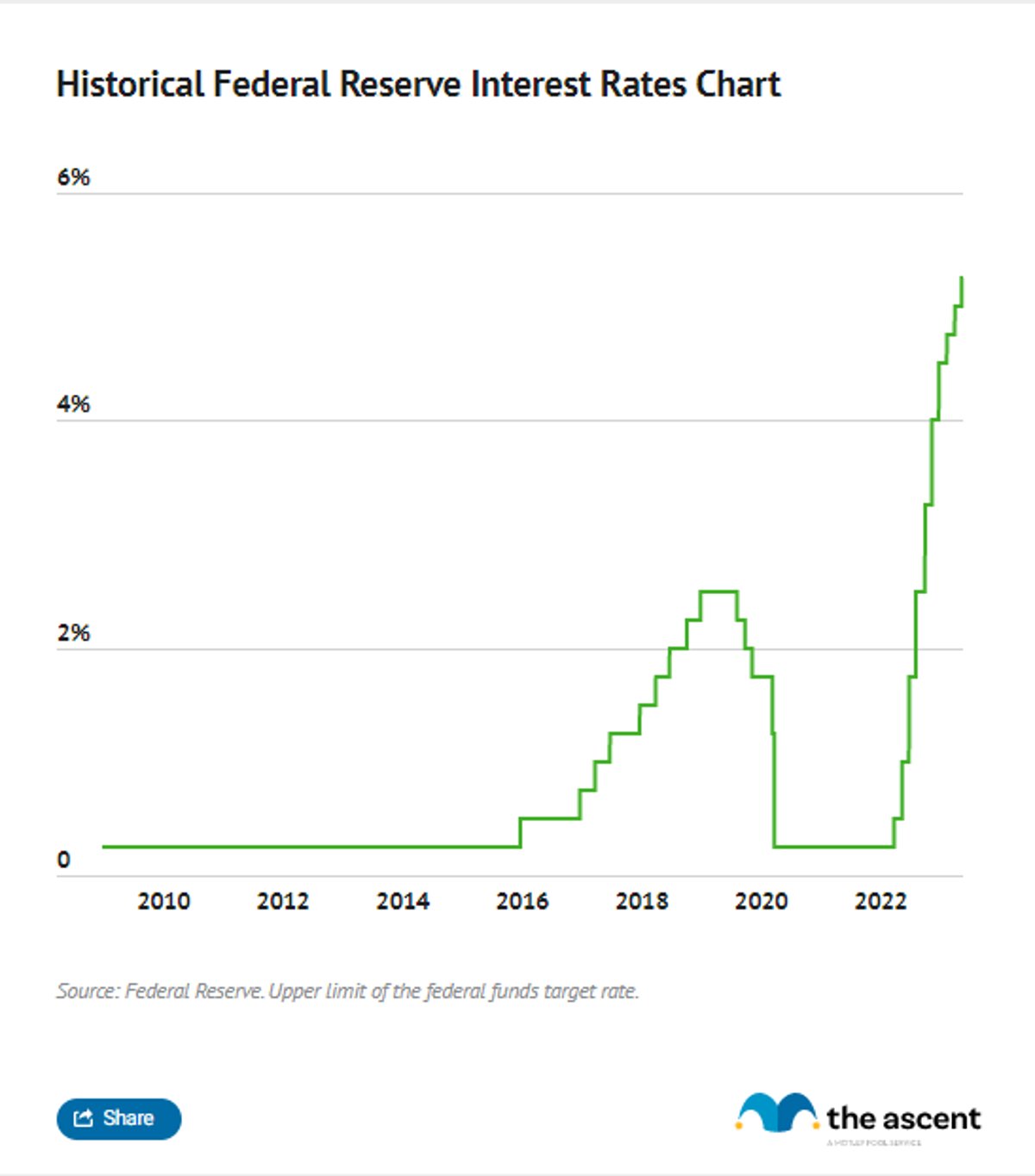

Interest rates aren't just plucked out of thin air. There's a whole system behind them. Central banks, like the Federal Reserve in the U.S., play a big role in setting interest rates. They use something called the benchmark interest rate, which serves as a guide for commercial banks when setting their own rates.

Here are a few factors that influence interest rates:

- Economic conditions: If the economy is booming, interest rates might go up to prevent overheating. Conversely, during a recession, rates might drop to encourage borrowing and spending.

- Inflation: Higher inflation usually leads to higher interest rates to keep prices in check.

- Credit risk: Borrowers with poor credit histories often face higher interest rates because they're considered riskier.

- Supply and demand: Just like any market, the availability of money and the demand for loans can affect interest rates.

So, next time you hear about the Fed raising or lowering rates, you'll know it's not just random—they're trying to keep the economy balanced.

Types of Interest Rates You Need to Know

Not all interest rates are created equal. There are different types of interest rates, and each one serves a specific purpose. Let's break them down:

Nominal Interest Rate

This is the basic interest rate you see advertised by banks and lenders. It's the rate before taking inflation into account. For example, if a savings account offers a 4% nominal interest rate, that's the rate you'll earn on your deposits.

Real Interest Rate

Now, here's where things get interesting. The real interest rate adjusts the nominal rate for inflation. If inflation is running at 2% and the nominal rate is 4%, the real interest rate is 2%. This gives you a better picture of how much your money is actually growing in value.

Fixed vs. Variable Interest Rates

When it comes to loans, you'll often encounter two types of interest rates:

- Fixed interest rates: These rates stay the same throughout the life of the loan. They're great if you want predictability in your payments.

- Variable interest rates: These rates can fluctuate based on market conditions. They might start lower than fixed rates, but they can increase over time, which could mean higher payments.

Choosing between fixed and variable rates depends on your financial situation and how comfortable you are with potential changes in your payments.

The Impact of Interest Rates on Your Wallet

Interest rates don't just exist in some far-off economic realm—they have a direct impact on your daily life. Let's explore how they affect different aspects of your finances.

Mortgage Rates

If you're planning to buy a house, mortgage rates are probably on your mind. A small change in interest rates can make a big difference in your monthly payments. For instance, a 0.5% increase in a 30-year mortgage could add hundreds of dollars to your total repayment over time. That's why it's crucial to shop around for the best rates and consider locking in a fixed rate if rates are low.

Credit Card Interest

Let's talk about something most of us deal with—credit cards. Credit card interest rates are often much higher than other types of loans, sometimes reaching 20% or more. If you carry a balance from month to month, those high rates can really add up. The best strategy is to pay off your balance in full each month to avoid interest charges altogether.

Savings Accounts

On the flip side, interest rates also affect how much you earn on your savings. High-yield savings accounts offer better returns than traditional accounts, but you might need to meet certain requirements, like maintaining a minimum balance. It's always a good idea to compare rates and find an account that works for you.

How to Take Advantage of Interest Rates

Now that you know how interest rates work, let's talk about how you can use them to your advantage. Here are a few tips:

Shop Around for the Best Rates

Don't settle for the first loan or savings account you find. Do your research and compare rates from different banks and lenders. You might be surprised at the differences you find.

Improve Your Credit Score

Your credit score plays a huge role in the interest rates you're offered. Pay your bills on time, keep your credit utilization low, and avoid opening too many accounts at once. These steps can help boost your score and get you better rates.

Consider Refinancing

If you already have a loan or mortgage, refinancing could save you money if interest rates have dropped since you took out the loan. Just make sure to factor in any fees or closing costs when deciding if refinancing is worth it.

Interest Rates and the Economy

Interest rates aren't just about personal finance—they also have a massive impact on the broader economy. When central banks adjust interest rates, they're trying to influence economic growth, inflation, and employment.

Expansionary Monetary Policy

When the economy is sluggish, central banks might lower interest rates to encourage borrowing and spending. This is known as expansionary monetary policy. Businesses can invest more, consumers can buy more, and the economy gets a boost.

Contractionary Monetary Policy

On the flip side, if the economy is overheating and inflation is rising too fast, central banks might raise interest rates. This is called contractionary monetary policy. Higher rates make borrowing more expensive, which slows down spending and helps bring inflation under control.

Common Misconceptions About Interest Rates

There are a few myths and misconceptions floating around about interest rates. Let's clear them up:

Myth: Lower Rates Always Mean Cheaper Loans

Not necessarily. While lower rates can reduce your monthly payments, they might also mean you end up paying more in interest over the life of the loan if the term is longer. Always calculate the total cost before signing on the dotted line.

Myth: Interest Rates Only Affect Borrowers

Wrong! Savers are affected too. When interest rates are low, you earn less on your savings. That's why it's important to find accounts that offer competitive rates, even in a low-rate environment.

Future Trends in Interest Rates

So, what's on the horizon for interest rates? Experts predict a few key trends:

Rising Rates

As economies recover from the pandemic, many central banks are expected to raise interest rates to combat inflation. This could mean higher borrowing costs for consumers and businesses alike.

Global Influence

Interest rates in one country can affect rates in others due to globalization. For example, if the U.S. raises rates, it can attract foreign investment, which might impact rates in other countries.

Final Thoughts

Interest rates might seem like a dry topic, but they're incredibly important for managing your finances. From mortgages to credit cards to savings accounts, understanding how interest rates work can help you make smarter decisions and save money in the long run.

So, here's what you can do next:

- Take a look at your current loans and see if you can refinance for better rates.

- Shop around for high-yield savings accounts to maximize your earnings.

- Keep an eye on economic news to stay informed about potential rate changes.

And remember, knowledge is power. The more you know about interest rates, the better equipped you'll be to navigate the world of finance. Now go out there and take control of your financial future!

Table of Contents

![Buying a Home? Mortgage Rate Guide for Singapore [2023]](https://blog.roshi.sg/wp-content/uploads/2022/08/Singapore-Home-Loan-Rates-2022.jpeg)